Losing a job or experiencing a sudden income reduction requires an immediate shift in how you handle your money. If you are trying to figure out what bills to pay first if you lose your job, you are not alone. Even a temporary drop in income can make every bill feel urgent.

The answer is not to keep paying everything the way you did before. When income changes, the order becomes more important.

There is a clear framework that protects stability first.

Your Priority Order When Income Changes

When income drops, the order is simple:

1. Cover the 4 Walls and essential medical needs

2. Make minimum payments if cash flow allows

3. Adjust everything else immediately

4. Then look at ways to bring in some income

This is the framework.

In this blog, we will walk through how to apply it.

Turn Off Autodrafts and Take Back Control

This is one of the first things to address.

When income drops, you cannot afford for money to leave your account automatically without a plan.

Go through your accounts and identify anything set to autodraft, especially:

- Credit cards

- Personal loans

- Subscription services

- Extra debt payments

Autodrafts are designed for convenience, not for income disruption.

You want to decide what gets paid and when.

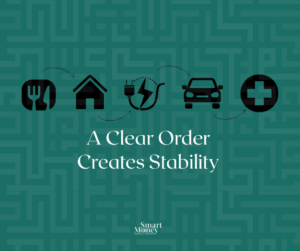

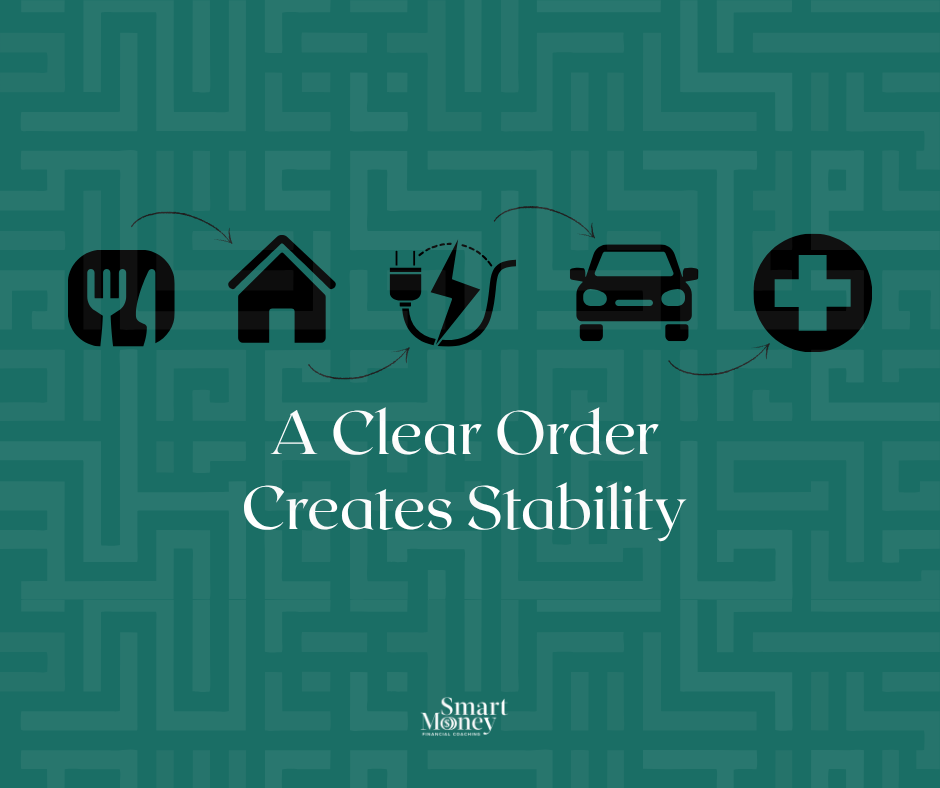

What Bills to Pay First If You Lose Your Job: Start with the 4 Walls

When income changes, your first priority is protecting the basics. Start with the 4 Walls.

The 4 Walls include:

Food

Groceries and basic household necessities. This is not the season for eating out or stocking up. It is about keeping food in the house.

Utilities

Electricity, water, gas, and basic phone service. These keep your home functioning and safe.

Housing

Rent or mortgage, along with homeowner’s or renter’s insurance.

Transportation

Car payment, fuel, and required insurance. If you need your vehicle to work or search for work, it remains essential.

In addition to the 4 Walls, protect essential medical needs. This includes prescriptions, necessary medical treatments, and ongoing care that affects health and safety.

These come before credit cards, personal loans, and extra debt payments.

Where Debt Fits When Deciding What Bills to Pay First

Once the essentials are covered, minimum payments come next if cash flow allows.

Some debt is tied to something essential, like your home or your vehicle. Other debt, like credit cards and most personal loans, is not.

That distinction matters.

If payments are missed on secured debt, you risk losing something you rely on. Unsecured debt does not come before the basics.

During a job loss or income reduction, the goal is not aggressive payoff. The goal is stability.

If minimum payments can be made without putting the 4 Walls at risk, that helps prevent additional complications.

If there is not enough income to cover minimum payments, contact lenders right away. Many have hardship options available.

Adjust Everything Else Immediately

This is the part you can control right away.

Be more intentional before you swipe, tap, or place an order online.

When income changes, spending needs to change with it. This is where many people lose clarity when deciding what bills to pay first if you lose your job.

This is the time to:

- Cancel or pause non-essential subscriptions

- Stop extra debt payments

- Pause investing contributions temporarily

- Reduce discretionary spending

- Reevaluate upcoming expenses

Preserving cash matters.

If possible, keep a small buffer in your checking account. Even a small cushion creates breathing room and helps prevent overdrafts.

Stability now prevents deeper problems later.

Stabilize First, Then Look at Income

Once your essentials are covered and spending is adjusted, you can start looking at ways to bring in some income.

That might look like part-time work, temporary opportunities, or flexible gig work that helps create some short-term stability.

It does not have to replace your full income. Bringing in something is often enough to take some pressure off while you stabilize.

Start by stabilizing what you have. Then look at what can be added.

How to Talk to Your Spouse During a Job Loss

A job loss or income reduction affects more than the numbers. It affects how both people feel.

Start with facts.

Review the income change together. Walk through the 4 Walls. Agree on what gets paid first. Then decide what pauses for now.

This is not a season for blame. It is a season for teamwork.

When both people understand the priorities, decisions feel more strategic and less personal.

I talk more about how couples can move forward even when priorities differ in Making Money Decisions as a Couple.

A Clear Order Creates Stability

Income disruption changes your numbers. It does not change your priorities.

The framework stays the same.

Food. Utilities. Housing. Transportation. Essential medical needs.

Then, make minimum payments if possible.

Then everything else.

When you know what bills to pay first if you lose your job, decisions become more straightforward.

If you want to read more about how my own family navigated significant income changes, you can read How We Survived a 50% Pay Cut.

If you want help applying this framework to your situation, you are welcome to schedule a complimentary call.

Frequently Asked Questions About What Bills to Pay First After Job Loss

Should I stop paying my credit cards if I lose my job?

Credit cards are unsecured debt. The priority is protecting food, housing, utilities, transportation, and essential medical needs. After that, minimum payments come next if possible.

What happens if I cannot afford my mortgage or rent?

Housing is part of the 4 Walls and should be prioritized. If you anticipate an issue, contact your landlord or mortgage company early. Many offer temporary relief options.

Should I use my emergency fund first?

If you have an emergency fund, this is what it is for. Use it to protect the 4 Walls and essential medical needs while you stabilize your income.

Following the steps above can help your emergency fund last longer.

Should I apply for unemployment immediately?

Yes. Apply as soon as possible. Starting early helps avoid delays in receiving benefits.

Should I keep contributing to retirement during a job loss?

Preserving cash flow comes first. Contributions can typically be paused temporarily while you stabilize essentials.